| | | | | | | | | | | | The old market saying “Sell in May, and go away” has once again failed to deliver. Instead of cooling off, markets have continued to defy gravity, pushing higher with remarkable consistency and resilience. The S&P 500 is a perfect illustration. The index has just completed its ninth consecutive week of gains, without a single negative week since our publication of March. But something important has changed. Despite the S&P 500 reaching record levels, equities are in fact becoming more affordable, not more expensive. Although this may seem counterintuitive, it is simply because company earnings have been growing even faster than stock prices. In fact, S&P 500 forward earnings have risen by almost 20% year over year, ie. twice the index performance since the begining of the year. In that sense, the lesson this year is clear. Not only it would have been wrong to “sell in May”, but “going away” by stepping aside is actually missing a rally that is supported by solid fundamentals. For now, the market is once again suggesting that investors should neither sell, nor go away. |

| | Stepping aside would actually be missing a rally that is supported by solid fundamentals. For now, the market is once again suggesting that investors should neither sell, nor go away |

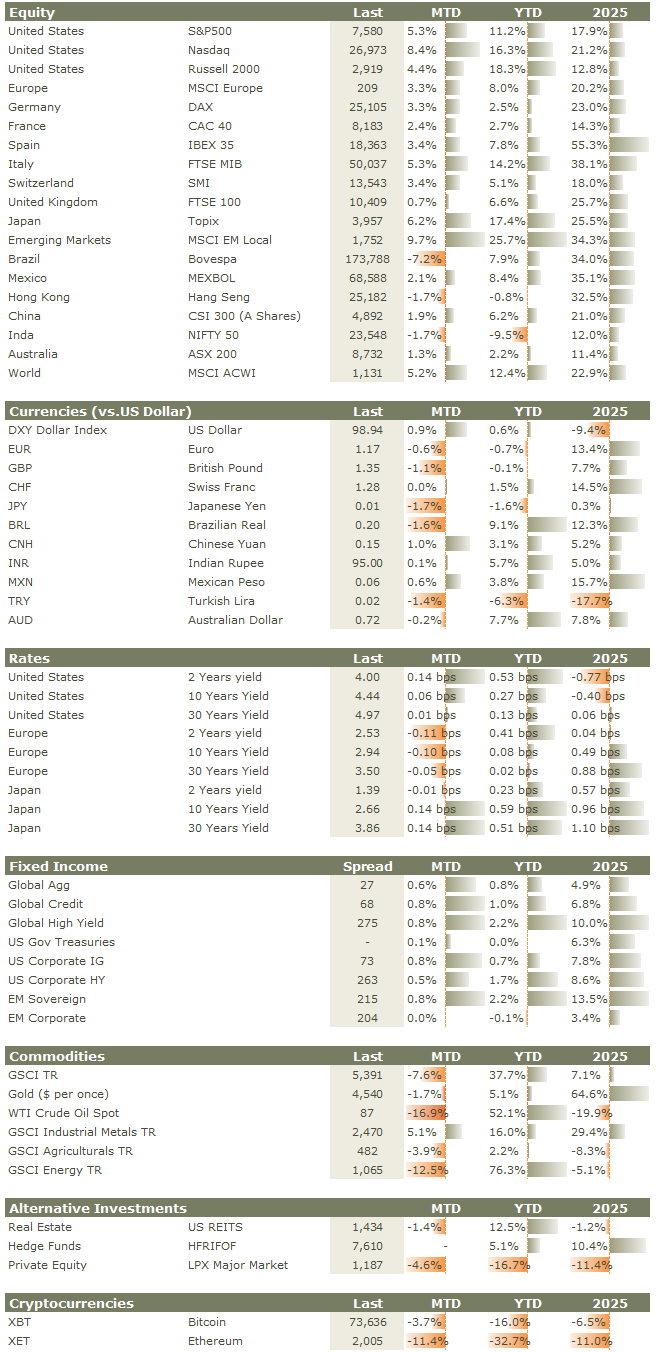

| | After April’s euphoria, markets extended their rebound into May, supported by strong corporate earnings, as mentioned earlier, but also by renewed hopes of de-escalation in the Middle East. Market leadership remained quite narrow, with gains once again concentrated in a handful of large-cap technology names, driving the Nasdaq (+8.4%) and the S&P 500 (+5.3%) to solid double-digit returns year-to-date. Emerging markets continued to outperform, led by exceptional gains in Korea (+28.5%) and Taiwan (+15%), both benefitting from their high exposure to the AI supply chain and sustained hyperscaler-driven investment demand. European equities (+3.3%) and China (+1.9%) also posted positive monthly performances. Japan also delivered a strong performance, with the Topix rising +6.2%, while Brazil stood out as one of the few negative performers over the month. Fixed income delivered positive returns overall, albeit with notable intra-month volatility as yields closely tracked energy market dynamics: the 10-year US Treasury briefly climbed above 4.6%, reaching multi-month highs before retracing toward month-end. Actually, the repricing in yield was broad-based, with the average 10-year borrowing cost for G7 governments approaching 4%, up from around 3.2% before the escalation of the Middle East conflict in late February. Lastly, Commodities declined over the month, weighed down primarily by energy, with oil prices (WTI, -16.9%) and Gold (-1.7%) both lower, while the US dollar index edged higher (+0.9%). |

| | Beyond the headlines from the Middle East, two main themes shaped market narratives over the month: corporate earnings and inflation. The US earnings season concluded on a particularly strong note, with average earnings growth in the US surpassing 25% and a large majority of companies delivering positive surprises, significantly improving visibility on corporate fundamentals. On the inflation front, several indicators pointed to mounting pressures across the global economy. Both US CPI (+3.8% YoY) and PPI (+6.0% YoY) came in above expectations, while Core PCE (+3.3% YoY), the Federal Reserve’s preferred gauge, reached its highest level since November 2023. These inflationary dynamics increasingly filtered into the real economy, compounded by a backdrop of geopolitical uncertainty, with consumer sentiment falling to the lowest level on record according to the University of Michigan survey. At the same time, the US labour market continued to exhibit resilience, consistent with a “low fire, low hire” environment, while growth showed early signs of moderation, with US GDP revised down to an annualized rate of 1.6%, from an initial estimate of 2%. On the monetary policy front, Kevin Warsh was officially confirmed as the next Federal Reserve Chairman (read our dedicated CIO Market Flash Note - "Inside the Powell - Warsh Transition"), while the ECB’s April meeting reinforced a distinctly hawkish stance, highlighting rising downside risks to growth alongside persistent upside risks to inflation. |

| | Refraining from unnecessary adjustments is not inertia, but a deliberate allocation choice, one that reflects the strength and resilience of well-constructed portfolios anchored in a long-term perspective |

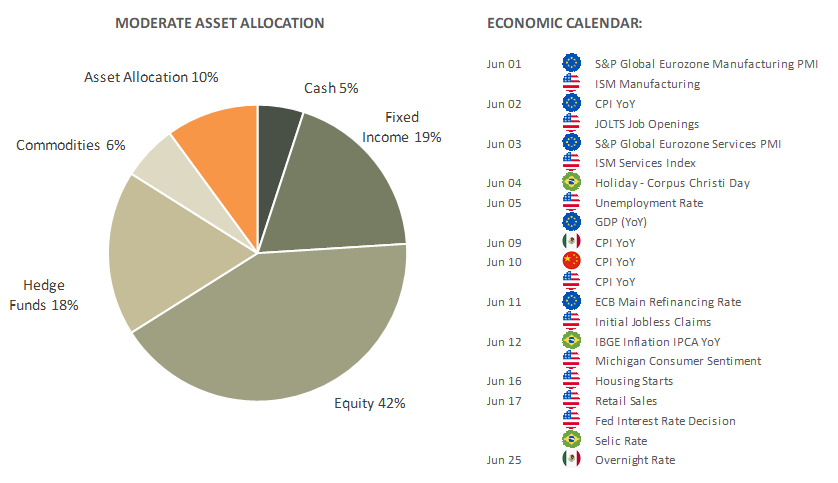

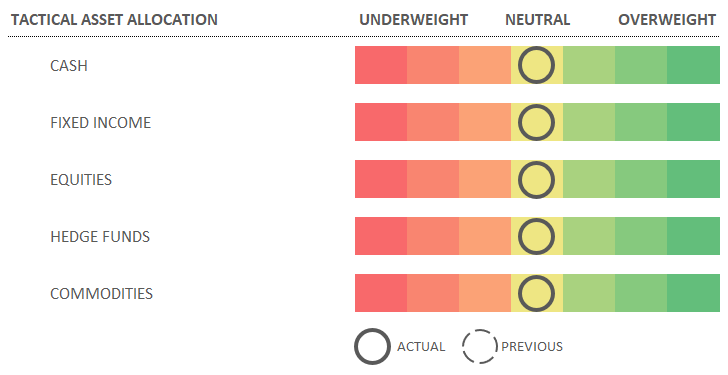

| | As we have been emphasizing in recent communications, discipline often matters more than activity. In periods such as today’s, refraining from unnecessary adjustments is not inertia but a deliberate allocation choice, one that reflects the strength and resilience of well-constructed portfolios anchored in a long-term perspective. This approach has proven rewarding in recent months. Accordingly, our core convictions remain unchanged. Within Fixed Income, we continue to favour credit quality while looking for pockets where we can still find value in a record tight credit spreads’ environment. In Equities, staying invested remains the right approach; however, selectively financing downside protection by capping part of the 12‑month upside meaningfully enhances the overall risk-adjusted profile of portfolios. In an environment marked by elevated equity-bond correlation, hedge funds have once again demonstrated their value as true diversifiers within our portfolios, combining resilience with still attractive upside participation. Finally, while recent six-month price action in gold has raised some concerns, we maintain our structural conviction: safe-haven scarcity, fiscal risks, and sustained central bank demand continue to provide long-term support, validating its strategic role as both a diversifier and a resilient store of value. |

| | | | | | | | | | | | | | | | |