2026 health insurance premiums: facts & figures

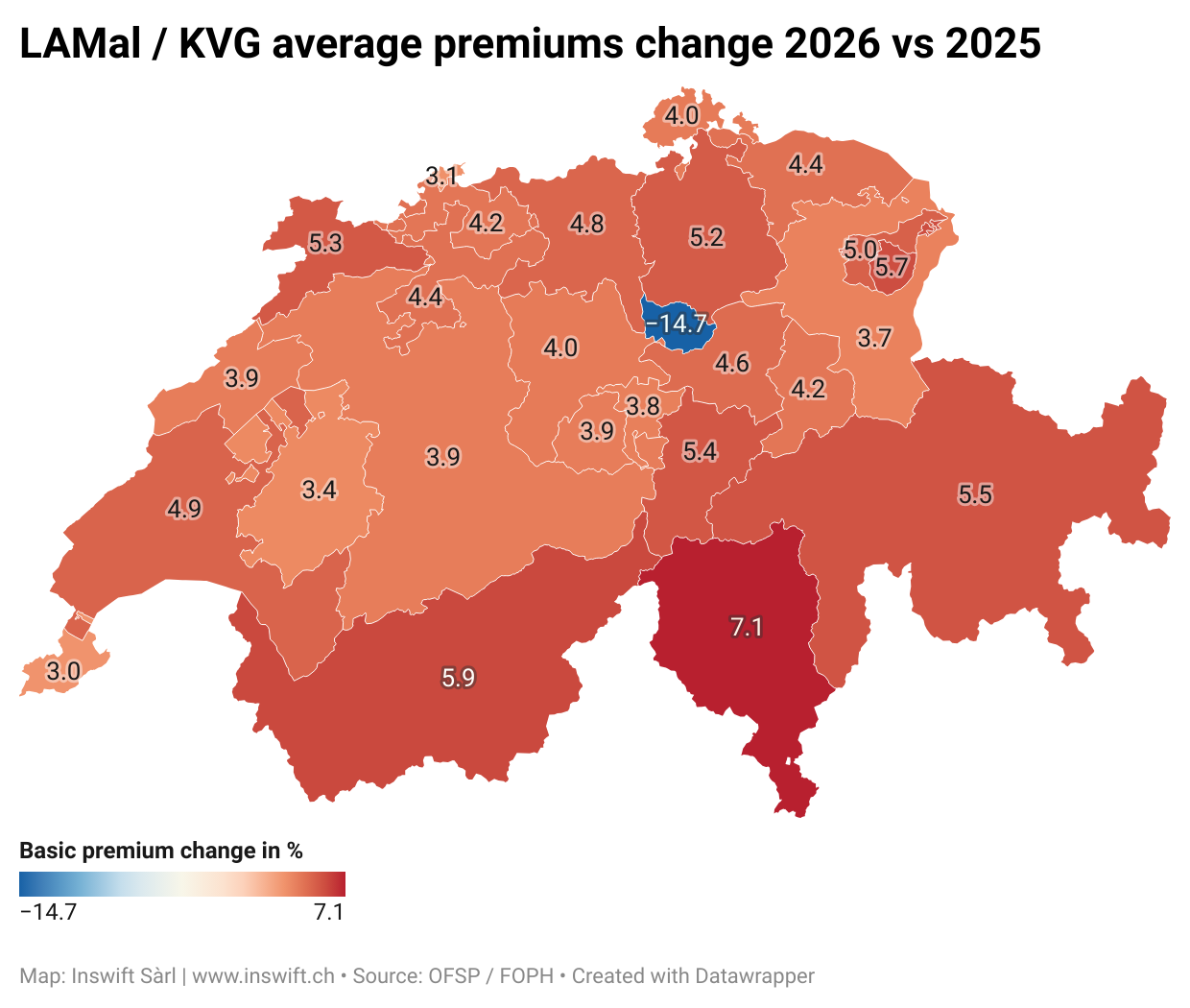

National average: 4.4%

Lowest increase: Geneva 3%

Highest increase: Ticino 7.1%

The odd one out: Zug -14.7%

Number of health insurance providers: 37

Some insurance companies are locally anchored while others have a national reach.

The parameters taken into account for your premium are your age, location, method of insurance, deductible and accident cover.

In 2026, it will be 30 years since the LAMal/KVG was introduced in Switzerland. In 1996, the average national premium was CHF 128. Thirty years onwards, the insurees are paying triple on average.

The basic health insurance premiums represent the main obligatory expense for Swiss households.

The reasons behind the continued increase over the decades: the unstoppable increase of healthcare costs. How is it then that Zug manages a substantial decrease for next year? The canton will pay 99% of its residents' hospital costs in 2026 and 2027.

If you wish to see what your new premium will be and how it compares with other options, we recommend the official Swiss Confederation premium checker: Priminfo.ch →

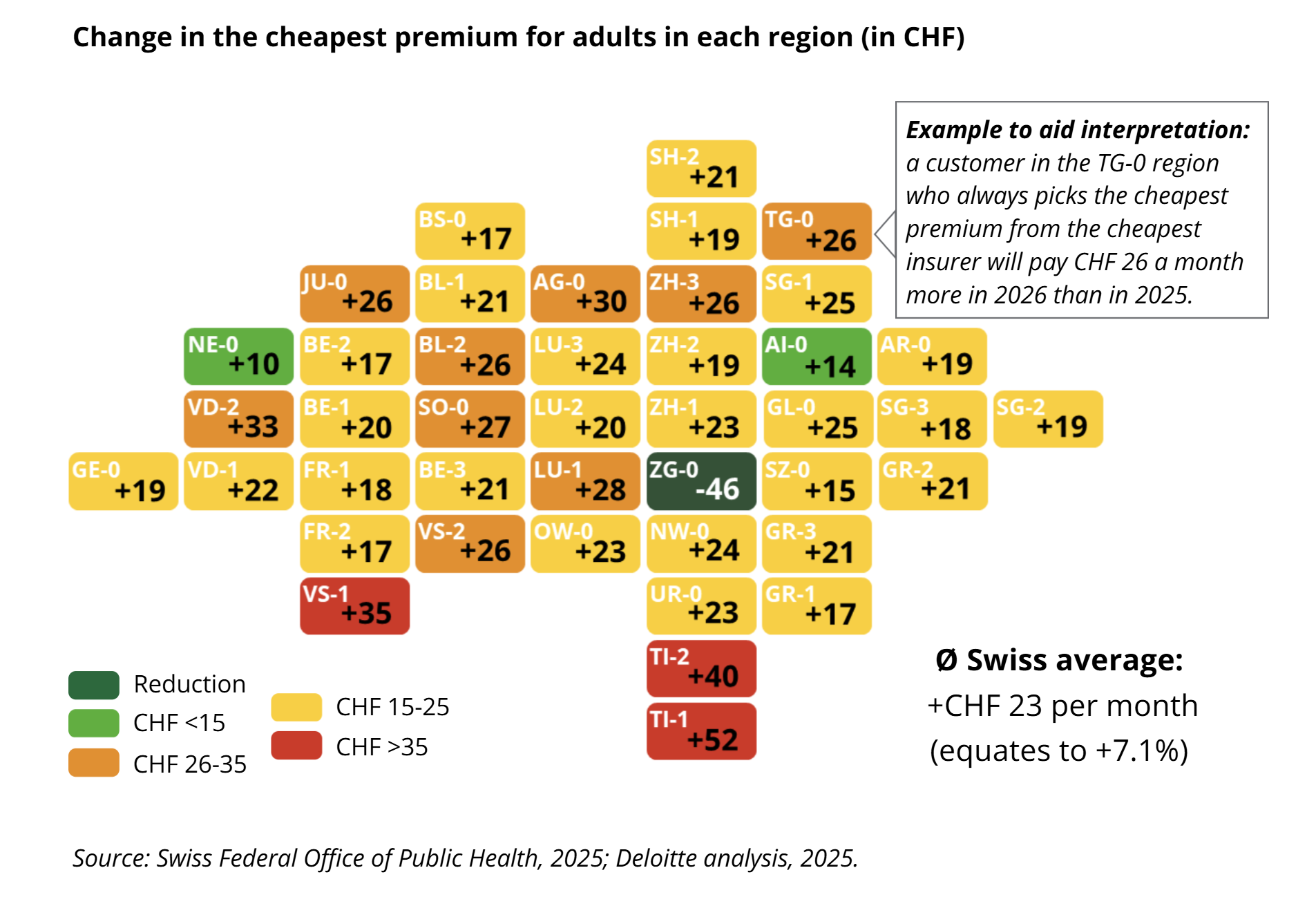

Deloitte Switzerland also analysed the new premiums and their study "has revealed that many policyholders paying the cheapest premiums on the market will face a 7 per cent hike on average, much higher than the officially communicated figure of 4.4 per cent," as shows the diagramme below, suggesting that "low-cost models in particular are coming under greater pressure". Read the full analysis →

Sources: FOPH, Le Temps, Deloitte Switzerland

|